You bought Bitcoin. Maybe Ethereum. Some SOL. You check the price every morning. The number goes up, goes down, and mostly you wait.

Here's the problem: your crypto isn't working for you. Banks pay 0.5% on savings. Your crypto exchange pays nothing. Meanwhile, there's an entire system where your assets could be earning income without being sold.

That system is DeFi.

What Is DeFi?

DeFi (Decentralized Finance) is a network of financial tools built on blockchain that lets you lend, borrow, and trade crypto without banks or brokers. Your assets stay in your wallet. You control everything. The protocols run on code, not executives.

No applications. No credit checks. No business hours. You deposit crypto, earn yield, withdraw whenever you want.

You can watch this YouTube video for a quick overview of how to deploy your crypto into DeFi.

Why Your Crypto Exchange Is the Wrong Place

Exchanges are hotels. You're renting a bed. The hotel owns the building.

When your Bitcoin sits on Coinbase or Binance, you don't actually control it. The exchange controls it. If they freeze withdrawals, you wait. If they go under, you're a creditor in bankruptcy court.

DeFi flips this. Your crypto stays in your wallet. Protocols interact with your wallet directly. You sign transactions. You approve everything. The code executes what you approved, nothing else.

Ownership is the entire point of crypto. Holding it on an exchange defeats the purpose.

Two Ways DeFi Actually Works

DeFi has a lot of noise. Most of it doesn't matter for beginners. Two mechanics matter: lending and liquidity pools.

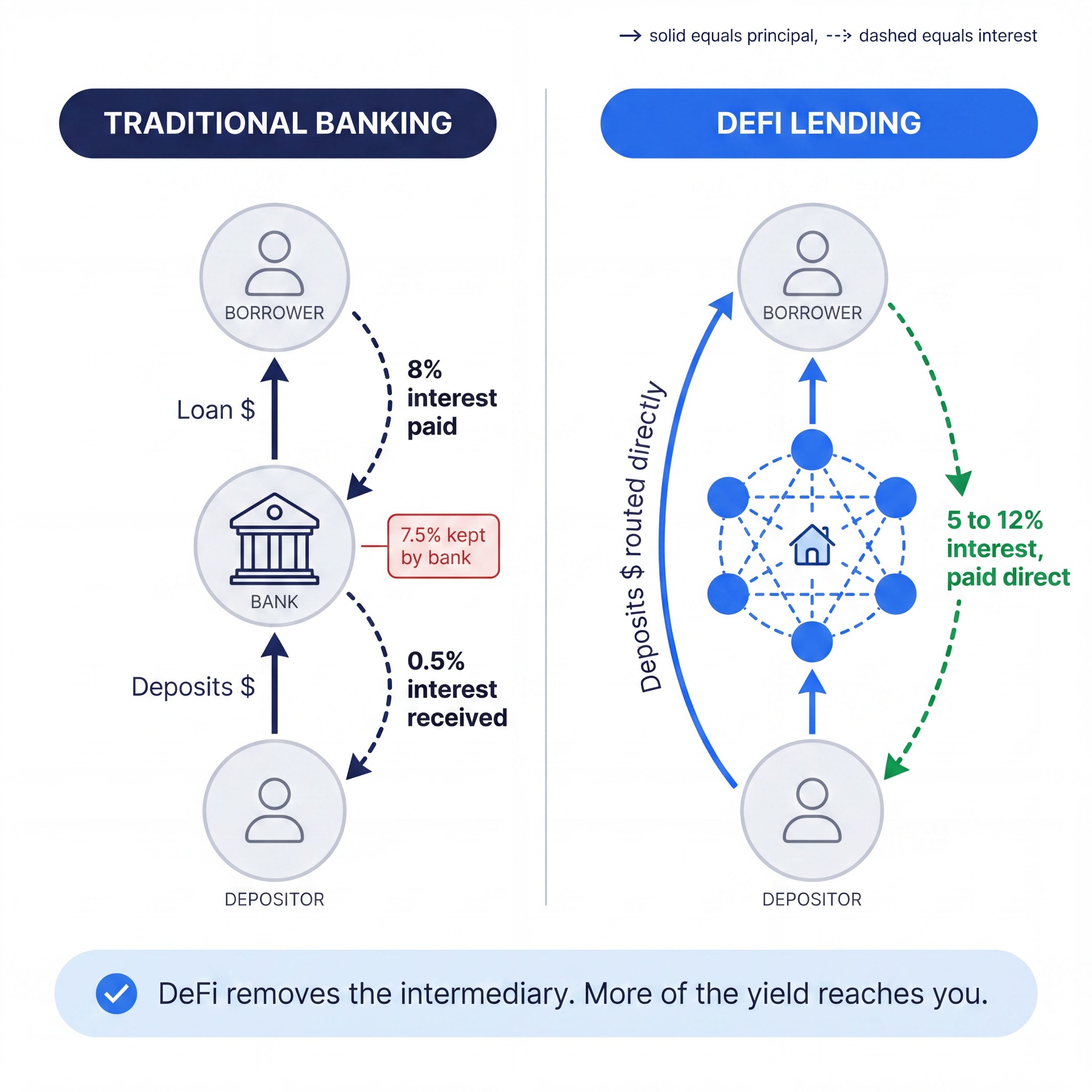

Traditional finance works like this: you deposit money, the bank lends it out, they pay you 0.5%, they charge borrowers 8%, they keep the 7.5% spread.

DeFi removes the bank. You deposit your crypto into a lending protocol Borrowers take loans directly from the pool. They pay interest. That interest goes to you.

In my analysis of recent data, stablecoin lending typically yields 5-8% annually in normal conditions. During high-demand periods (bull markets, when traders pile into positions), rates climb to 10-12% or higher. Your BTC, ETH, or SOL sits in the pool, borrowers pay to use it, you collect the interest continuously.

The safety mechanism: every loan is overcollateralized. A borrower must lock up $150 worth of crypto to borrow $100. If the collateral value drops too far, the protocol automatically sells it and repays lenders. You don't lose principal from defaults. The code enforces this at the smart contract level.

This is why lending is the safest entry point into DeFi. The downside risk is managed by the protocol itself, and you earn steady income regardless of price movements.

Liquidity Pools: Be the Exchange

Every trade on a decentralized exchange needs liquidity. When someone swaps ETH for USDC, that swap pulls from a pool of ETH and USDC deposited by liquidity providers.

You become the liquidity provider. You deposit both tokens into the pool. Every swap through that pool pays a fee (usually 0.01% to 1% per trade). That fee gets split among all liquidity providers based on their share of the pool.

Think of it like owning a currency exchange booth at an airport. You don't care which direction people convert. You earn the spread on every transaction. More volume means more fees, regardless of which way price moves.

The newer version, called concentrated liquidity, lets you focus your capital in a specific price range. Instead of spreading $10,000 across all possible prices from $0 to infinity, you focus it between $2,500 and $3,500 if ETH is trading at $3,000. Your capital becomes up to 4,000x more efficient. The same $10,000 earns fees that would previously require millions.

This is where the higher monthly returns come from. You're not just providing liquidity anymore. You're providing it exactly where the trading activity happens.

The Real Numbers on Liquidity Pools

Over the past 18 months, we've tracked concentrated liquidity positions across 17 different market scenarios: bull runs, bear markets, sideways chop, high volatility, low volatility. The data consistently shows that properly managed positions generate 6-12% monthly returns when markets are stable to moderately volatile.

This isn't speculation on price. This is fee income from trading volume.

The actual yields we've seen, both from our own positions and from students running the same strategies, fall within this range. Positions are tracked in real time, and people share their results as they go. The 6-12% spread isn't a projection. It's what's happening.

The range depends on two things: how active the market is, and how you manage the position.

Passive, wide ranges on stable pairs like USDC/USDT sit at the low end (6-7% monthly). You set it up, check it weekly, rebalance when price moves out of range. Minimal time commitment.

Tighter ranges on high-volume pairs like ETH/USDC or SOL/USDC with regular rebalancing reach the high end (6-12% monthly). This requires daily monitoring and more frequent adjustments. More work, higher potential income.

You can watch this YouTube video for a breakdown of how to increase cashflow using different strategies and DeFi protocols.

Compare this to traditional finance. A high-yield savings account pays 4-5% annually. A corporate bond might pay 6% annually. DeFi liquidity pools, done right, can deliver that in a single month.

The reason: trading volume in crypto is massive. On February 15, 2026, Uniswap alone processed $2.1 billion in trading volume. Every swap pays a fee. Liquidity providers collect those fees continuously, 24/7, across all time zones. No market hours. No weekends off.

The key is understanding that this isn't free money. You're providing a service (liquidity for traders) and getting paid for it (swap fees). The better you position your liquidity, the more fees you collect.

What About Risk?

DeFi yields are higher because real risks exist. But they can be managed.

Smart contract risk Protocols run on code. Code can have bugs. Use only battle-tested protocols with billions locked and multiple security audits. Aave has been running since 2017. Uniswap has processed over $2 trillion in volume since launch.

Price movement risk When you provide liquidity and price moves, your position rebalances. You end up with more of the cheaper token, less of the expensive one. Fee income must exceed this for the strategy to profit. Wider ranges and proper positioning minimize this issue.

Market volatility Stablecoin strategies (USDC/USDT) avoid price risk entirely. Volatile asset strategies (ETH/SOL pools) expose you to price swings. Choose based on your comfort level.

Start simple. Stablecoin lending is the safest entry point. Learn the mechanics. Then explore liquidity pools when you're ready. There are step-by-step resources that walk through everything, from wallet setup to position monitoring.

The discipline: never deploy capital you can't afford to lose while learning. Use proven protocols only. Start small until you understand how everything works.

Your Crypto Is an Asset. Assets Should Work.

The infrastructure exists. The yields are real. The mechanics can be learned. DeFihouse breaks down the full system through video lessons that walk through each strategy step by step, from the basics of lending to more advanced approaches like liquidity provision and risk management.